16. Random Matrices¶

A matrix is interesting only in those ways it fails to look like a random matrix.

A random matrix is a matrix whose entries are random, i.e., random draws from some distribution(s). More precisely, the entries of a random matrix are random variables, which means their values are determined probabilistically.

You would expect that a random matrix must no covariance structure, because it is random. In fact, random matrices have a covariance structure described by the Marchenko-Pastur distribution.

In this lecture, we start with the maths, and then we look at a random matrix example that arises in finance. Finally, we illustrate a denoising technique based on a medical imaging example.

A useful reference on the topic and the importance of random matrix in machine learning are:

For a connection between random matrices results in spin glasses and machine learning see:

For insights from both physics and finance, see:

16.1. Wigner Semicircle Law¶

Consider a matrix \(M\) belonging to the Gaussian Orthogonal Ensemble (GOE).

Such a matrix \(M\) can be a real symmetric \(n \times n\) matrix with i.i.d. entries \(M_{ij}\) drawn from a normal distribution with mean 0 and variance 1.

Let us compute such a matrix.

[5]:

import numpy as np

import matplotlib.pyplot as plt

n = 50

A = np.random.randn(n, n)

M = (A + A.T) / np.sqrt(2 * n)

plt.figure(figsize=(5,5))

plt.imshow(M, cmap='viridis')

plt.colorbar(label='Value', shrink=0.8)

plt.title('Random GOE Matrix')

plt.xlabel('Column Index')

plt.ylabel('Row Index')

plt.show()

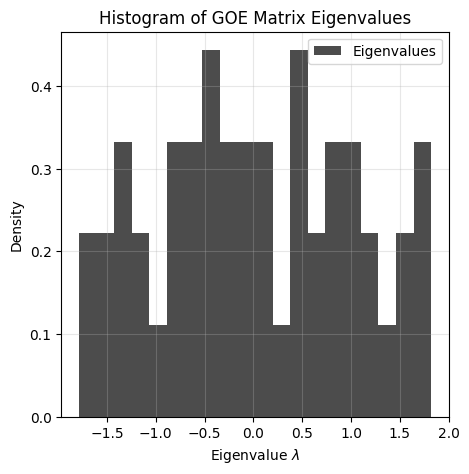

We compute the eigenvalues of \(M\), i.e., \(\lambda_1, \ldots, \lambda_n\) such that \(M v_i = \lambda_i v_i\) for \(i=1,\ldots, n\), where \(v_1, \ldots, v_n\) are the eigenvectors of \(M\).

[9]:

lambdas = np.linalg.eigvalsh(M)

len(lambdas)

[9]:

50

[11]:

lambdas

[11]:

array([-1.78831596, -1.66285061, -1.60735989, -1.478767 , -1.37076632,

-1.28266936, -1.26073123, -1.17522307, -1.15078943, -1.0505597 ,

-0.87587328, -0.82994073, -0.81216264, -0.69627856, -0.63556949,

-0.60146074, -0.5174084 , -0.49149304, -0.42805175, -0.34783377,

-0.30842303, -0.18600724, -0.16910437, -0.0798577 , -0.06882297,

-0.03037273, 0.10134173, 0.12347385, 0.19636835, 0.33194403,

0.39814771, 0.40461385, 0.48102878, 0.5181245 , 0.57489408,

0.60581731, 0.74318659, 0.74941497, 0.83245446, 0.99281742,

1.04225235, 1.06837886, 1.18588169, 1.2323374 , 1.40538206,

1.46164366, 1.54461226, 1.65577622, 1.73020455, 1.8206828 ])

lambdas is an array of length n containing the eigenvalues of \(M\). We can present the eigenvalues in a histogram. This histogram is sometimes referred to as the empirical eigenvalue distribution.

[12]:

plt.figure(figsize=(5,5))

plt.hist(lambdas, bins=20, density=True, alpha=0.7, color='black', label='Eigenvalues')

plt.title('Histogram of GOE Matrix Eigenvalues')

plt.xlabel(r'Eigenvalue $\lambda$')

plt.ylabel('Density')

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

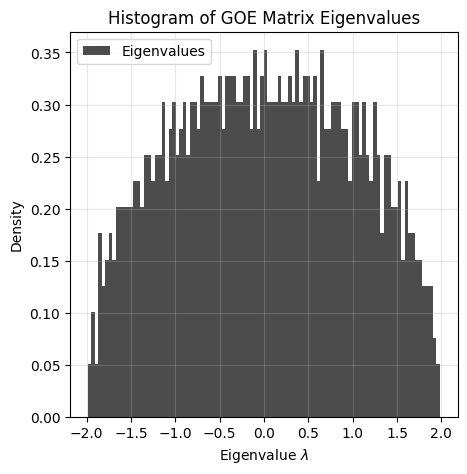

Let us now consider the limiting case as \(n \to \infty\).

For instance, pick \(n=1000\).

[13]:

%%time

n = 1000

A = np.random.randn(n, n)

M = (A + A.T) / np.sqrt(2 * n)

lambdas = np.linalg.eigvalsh(M)

CPU times: user 161 ms, sys: 38.9 ms, total: 200 ms

Wall time: 164 ms

[14]:

plt.figure(figsize=(5,5))

plt.hist(lambdas, bins=100, density=True, alpha=0.7, color='black', label='Eigenvalues')

plt.title('Histogram of GOE Matrix Eigenvalues')

plt.xlabel(r'Eigenvalue $\lambda$')

plt.ylabel('Density')

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

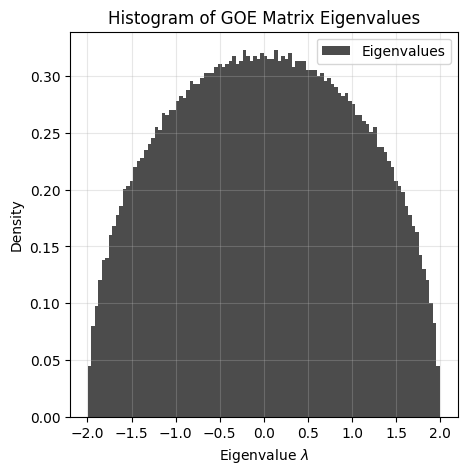

n = 10000, so the matrix is 10000 by 10000

[4]:

%%time

n = 10000

A = np.random.randn(n, n)

M = (A + A.T) / np.sqrt(2 * n)

lambdas = np.linalg.eigvalsh(M)

CPU times: user 6min 38s, sys: 42.3 s, total: 7min 21s

Wall time: 4min 18s

[6]:

plt.figure(figsize=(5,5))

plt.hist(lambdas, bins=100, density=True, alpha=0.7, color='black', label='Eigenvalues')

plt.title('Histogram of GOE Matrix Eigenvalues')

plt.xlabel(r'Eigenvalue $\lambda$')

plt.ylabel('Density')

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

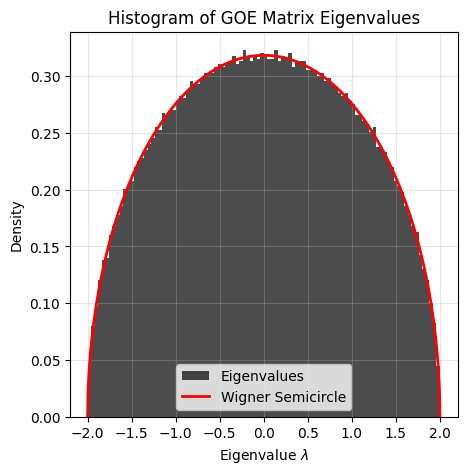

The histogram converges to a semicircle. The eigenvalues are distributed according to the Wigner semicircle distribution:

Here with \(R=2\).

Note that if the standard deviation of the normal distribution is \(\sigma\), then the semicircle radius is \(R = 2 \sigma\).

[7]:

plt.figure(figsize=(5,5))

plt.hist(lambdas, bins=100, density=True, alpha=0.7, color='black', label='Eigenvalues')

x = np.linspace(-2, 2, 1000)

y = 2/(np.pi*4) * np.sqrt(4 - x**2) # R=2 case

plt.plot(x, y, 'r-', label='Wigner Semicircle', lw=2)

plt.title('Histogram of GOE Matrix Eigenvalues')

plt.xlabel(r'Eigenvalue $\lambda$')

plt.ylabel('Density')

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

This property was discovered by Eugene Wigner in the 1950s, working on nuclear physics (more precisely the spaces between the energy levels of heavy nuclei). See Wigner surmise for more details.

Wigner’s insight was as follows:

Perhaps I am now too courageous when I try to guess the distribution of the distances between successive levels (of energies of heavy nuclei). Theoretically, the situation is quite simple if one attacks the problem in a simpleminded fashion. The question is simply what are the distances of the characteristic values of a symmetric matrix with random coefficients. (Wigner, 1956)

16.2. Wishart Matrices¶

This ensemble of matrices is called the Wishart Ensemble and named after the British statistician John Wishart.

16.2.1. Sample Covariance Matrices¶

Consider \(T\) observations \(\mathbf{x}_1, \ldots, \mathbf{x}_T\), with \(\mathbf{x}_t \in \mathbb{R}^N\).

The sample covariance matrix (SCM) is defined as:

It is of size \(N \times N\). With \(\mathbf{H}\) the matrix of observations (the data matrix), i.e., \(\mathbf{H} = [\mathbf{x}_1, \ldots, \mathbf{x}_T]\) of size \(N \times T\), we can write:

You can show that \(\mathbf{E}\) is symmetric and positive semidefinite, and therefore all its eigenvalues are real and non-negative: \(\lambda_1, \ldots, \lambda_N \geq 0\).

16.2.2. Wishart Ensemble¶

When the entries of \(\mathbf{H}\) are i.i.d. normal random variables, then \(\mathbf{E}\) is a Wishart matrix belonging to the Wishart Ensemble. Moreover, the probability distribution defined over the space of \(\mathbf{E}\)’s is known as the Wishart distribution.

An important parameter to characterize these matrices is the ratio \(q = N/T\).

When \(q \to 0\), the number of observations \(T\) is much larger than the number of features \(N\), and one can faithfully reconstruct the true covariance matrix from the SCM.

But when \(q=\mathcal{O}(1)\), the number of observations is of the same order as the number of features, and the SCM is very distorted version of the true covariance matrix.

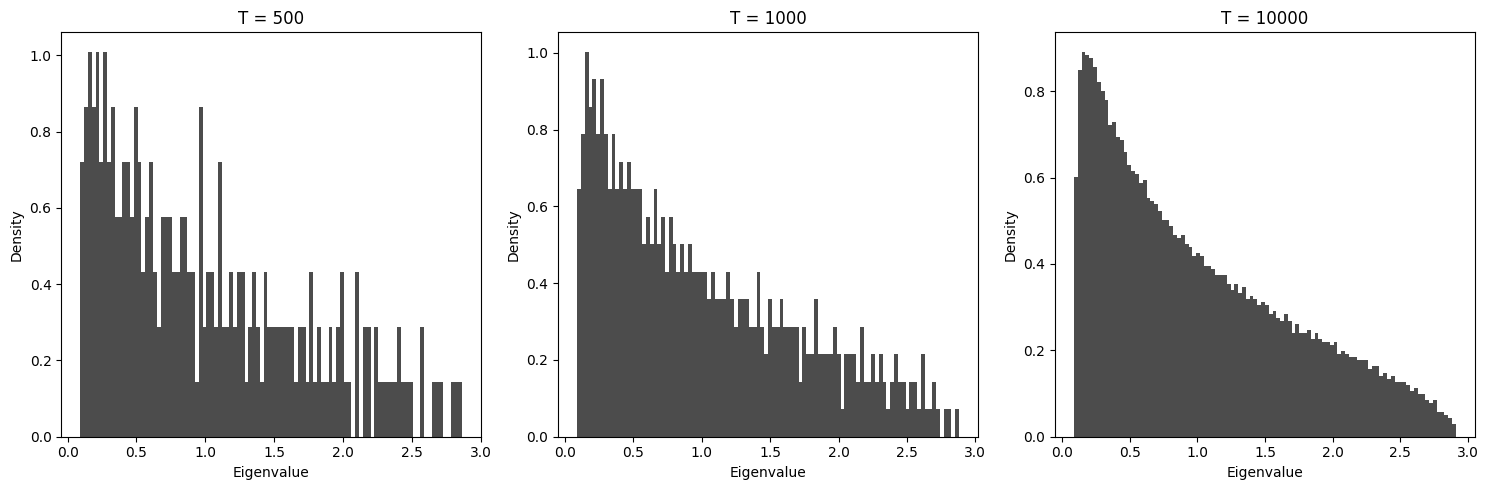

Let us fix \(q=1/2\) and look at the histogram of the eigenvalues of a Wishart matrix, as we increase the number of observations \(T\).

[1]:

import numpy as np

import matplotlib.pyplot as plt

q = 1 / 2

fig, ax = plt.subplots(1, 3, figsize=(15, 5)) # Larger figure size for better spacing

# Define the different values of T to loop over

Ts = [500, 1000, 10000]

for i, T in enumerate(Ts):

N = int(q * T)

H = np.random.randn(N, T)

E = H @ H.T / T

lambdas = np.linalg.eigvalsh(E)

# Plot the histogram of eigenvalues

ax[i].hist(lambdas, bins=100, density=True, alpha=0.7, color='black')

ax[i].set_title(f'T = {T}', fontsize=12)

ax[i].set_xlabel('Eigenvalue', fontsize=10)

ax[i].set_ylabel('Density', fontsize=10)

# Adjust layout

plt.tight_layout()

plt.show()

We see that for large \(T\) the histogram converges to a seemingly continuous distribution.

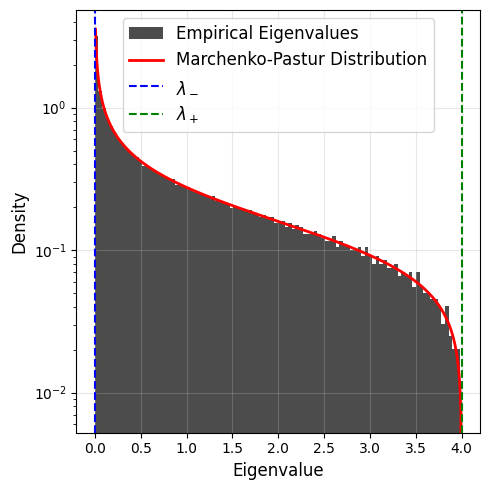

16.3. Marchenko Pastur Distribution¶

The Marchenko Pastur distribution is a distribution of eigenvalues. The formula is:

where \(\lambda_+, \lambda_-\) are given by:

16.3.1. Marchenko Pastur Law¶

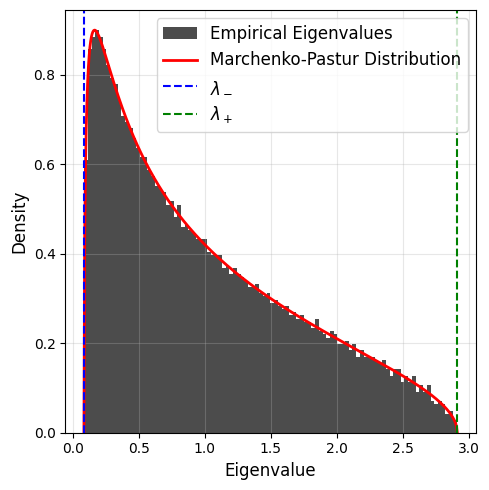

The Marchenko Pastur law implies that when both \(N\) and \(T\) are large, the empirical eigenvalue distribution of Wishart matrices converges to the Marchenko Pastur distribution with \(q=N/T\).

We can verify this with our previous example where we fixed \(q=1/2\).

[3]:

import numpy as np

import matplotlib.pyplot as plt

# Parameters

q = 1 / 2

T = 10000

N = int(q * T)

# Generate the random matrix and compute eigenvalues

H = np.random.randn(N, T)

E = H @ H.T / T

lambdas = np.linalg.eigvalsh(E)

# Calculate Marchenko-Pastur distribution

lambda_minus = (1 - np.sqrt(q))**2

lambda_plus = (1 + np.sqrt(q))**2

x = np.linspace(lambda_minus, lambda_plus, 500)

mp_density = (1 / (2 * np.pi * q * x)) * np.sqrt((lambda_plus - x) * (x - lambda_minus))

mp_density = np.where((x >= lambda_minus) & (x <= lambda_plus), mp_density, 0) # Set density to 0 outside the range

[6]:

# Plotting

plt.figure(figsize=(5, 5))

plt.hist(lambdas, bins=100, density=True, alpha=0.7, color='black', label='Empirical Eigenvalues')

plt.plot(x, mp_density, color='red', linewidth=2, label='Marchenko-Pastur Distribution')

plt.axvline(lambda_minus, color='blue', linestyle='--', label=r'$\lambda_-$')

plt.axvline(lambda_plus, color='green', linestyle='--', label=r'$\lambda_+$')

# Labels and legend

# plt.title(f'Eigenvalue Distribution and Marchenko-Pastur Law (T={T})', fontsize=14)

plt.xlabel('Eigenvalue', fontsize=12)

plt.ylabel('Density', fontsize=12)

plt.legend(fontsize=12)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

Let us now look at different values of \(q\).

Case q=2:

[7]:

import numpy as np

import matplotlib.pyplot as plt

# Parameters

q = 2

T = 5000

N = int(q * T)

# Generate the random matrix and compute eigenvalues

H = np.random.randn(N, T)

E = H @ H.T / T

lambdas = np.linalg.eigvalsh(E)

# Calculate Marchenko-Pastur distribution

lambda_minus = (1 - np.sqrt(q))**2

lambda_plus = (1 + np.sqrt(q))**2

x = np.linspace(lambda_minus, lambda_plus, 500)

mp_density = (1 / (2 * np.pi * q * x)) * np.sqrt((lambda_plus - x) * (x - lambda_minus))

mp_density = np.where((x >= lambda_minus) & (x <= lambda_plus), mp_density, 0) # Set density to 0 outside the range

[23]:

# Plotting

plt.figure(figsize=(5, 5))

hist_vals, bins, _ = plt.hist(lambdas, bins=100, density=True, alpha=0.7, color='black', label='Empirical Eigenvalues')

plt.plot(x, mp_density, color='red', linewidth=2, label='Marchenko-Pastur Distribution')

plt.axvline(lambda_minus, color='blue', linestyle='--', label=r'$\lambda_-$')

plt.axvline(lambda_plus, color='green', linestyle='--', label=r'$\lambda_+$')

zero_mass = (q - 1) / q # Amplitude of delta function at zero

bin_width = bins[1] - bins[0]

plt.bar(0, zero_mass/bin_width, width=bin_width, color='red', alpha=0.7, label=r'Mass at origin')

plt.yscale('log')

# Labels and legend

# plt.title(f'Eigenvalue Distribution and Marchenko-Pastur Law (T={T}, q={q})', fontsize=14)

plt.xlabel('Eigenvalue', fontsize=12)

plt.ylabel('Density', fontsize=12)

plt.legend(fontsize=12)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

When \(q>1\), the Marchenko Pastur distribution has a mass at the origin, its amplitude is given by \((q-1)/q\) (times a Dirac delta function).

Case q=1:

[24]:

import numpy as np

import matplotlib.pyplot as plt

# Parameters

q = 1

T = 5000

N = int(q * T)

# Generate the random matrix and compute eigenvalues

H = np.random.randn(N, T)

E = H @ H.T / T

lambdas = np.linalg.eigvalsh(E)

# Calculate Marchenko-Pastur distribution

lambda_minus = (1 - np.sqrt(q))**2

lambda_plus = (1 + np.sqrt(q))**2

x = np.linspace(lambda_minus, lambda_plus, 500)

mp_density = (1 / (2 * np.pi * q * x)) * np.sqrt((lambda_plus - x) * (x - lambda_minus))

mp_density = np.where((x >= lambda_minus) & (x <= lambda_plus), mp_density, 0) # Set density to 0 outside the range

/var/folders/h0/4_tf3pcn1h32ks9grh325v400000gn/T/ipykernel_61003/3342109622.py:18: RuntimeWarning: divide by zero encountered in divide

mp_density = (1 / (2 * np.pi * q * x)) * np.sqrt((lambda_plus - x) * (x - lambda_minus))

/var/folders/h0/4_tf3pcn1h32ks9grh325v400000gn/T/ipykernel_61003/3342109622.py:18: RuntimeWarning: invalid value encountered in multiply

mp_density = (1 / (2 * np.pi * q * x)) * np.sqrt((lambda_plus - x) * (x - lambda_minus))

[25]:

# Plotting

plt.figure(figsize=(5, 5))

hist_vals, bins, _ = plt.hist(lambdas, bins=100, density=True, alpha=0.7, color='black', label='Empirical Eigenvalues')

plt.plot(x, mp_density, color='red', linewidth=2, label='Marchenko-Pastur Distribution')

plt.axvline(lambda_minus, color='blue', linestyle='--', label=r'$\lambda_-$')

plt.axvline(lambda_plus, color='green', linestyle='--', label=r'$\lambda_+$')

plt.yscale('log')

# Labels and legend

# plt.title(f'Eigenvalue Distribution and Marchenko-Pastur Law (T={T}, q={q})', fontsize=14)

plt.xlabel('Eigenvalue', fontsize=12)

plt.ylabel('Density', fontsize=12)

plt.legend(fontsize=12)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

When \(q=1\), the Marchenko Pastur distribution has a singularity at the origin. It diverges as \(\sim 1/\sqrt{\lambda}\). In fact, in this case, the matrix \(\mathbf{H}\) is a Wigner matrix with its eigenvalues distributed according to the Wigner semicircle distribution, and the corresponding distribution of the square of these eigenvalues (i.e., the eigenvalues of \(\mathbf{E}\)) is distributed according to the distribution illustrated above.

16.3.2. Non-unit variance¶

When the variance of the entries of \(\mathbf{H}\) is not 1, the Marchenko Pastur distribution is given by:

where \(\lambda_\pm = (1 \pm \sqrt{q})^2 \sigma^2\).

16.3.3. Universality¶

In fact, the Marchenko Pastur distribution is universal in the sense that it does not depend on the specific distribution of the entries of \(\mathbf{H}\).

The theorem is due to Marchenko and Pastur (1967) and it states that:

Let \(\mathbf{H}\) be an \(N \times T\) random matrix with i.i.d. entries \(x_{ij}\) that verify:

\[\mathbb{E}[x_{ij}] = 0, \quad \mathbb{E}[x_{ij}^2] = 1 \quad \text{and} \quad \mathbb{E}[x_{ij}^4] < \infty.\]Then when \(N, T \to \infty\), the empirical eigenvalue distribution of \(\mathbf{E} = \frac{1}{T} \mathbf{H} \mathbf{H}^T\) converges to the Marchenko Pastur distribution with \(q=N/T\).

Thus, the entries do not need to be Gaussian, as long as the above moment conditions are verified.

The most important feature predicted by the Marchenko Pastur law is that the eigenvalues live in a finite, well defined interval.

The Marchenko Pastur law is an extremely important result, with applications that continue to be discovered. With this result, random matrix theory took a new dimension.

16.4. Application to Finance¶

Understanding correlations between stocks is maybe the most important problem in finance. Thus, measuring or estimating correlations between stock prices is crucial. This generally underlies risk management and portfolio allocation strategies.

The question every analyst wants to answer is: Given a set of financial assets (say a set of stocks), characterized by their average returns and risk (i.e., volatility), what is the optimal weight for each asset such that the portfolio provides the best return for a fixed level of risk?

This question can not be answered without a reliable determination of the stock correlation matrix.

For \(N\) stocks, the correlation matrix is of size \(N \times N\) and has \(N(N-1)/2\) free parameters. It has to be determined from \(N\) time series of length \(T\).

For instance, for \(N=400\) stocks of the S&P 500 index this means \(\approx 80,000\) parameters to estimate. Say we have 4 years of data, i.e., \(N\) time series of length \(T=252 \times 4 = 1008\) trading days. In this case, \(T\) is not very large compared to \(N\), and the estimation of the correlation matrix ought to be noisy, i.e, random to a large extent. In this case, the structure of the correlation matrix is actually dominated by noise.

In principle, the eigenvectors of the correlation matrix that correspond to the smallest eigenvalues are the ones that we should use to construct the portfolio that maximizes the return-to-risk ratio. However, these eigenvectors are also the most affected by noise. Therefore, it is important to separate the signal (eigenvectors that have real information) from the noise.

16.4.1. Correlation of S&P 500 components¶

Let us load the daily returns of the S&P 500 components.

[2]:

import pandas as pd

link = (

"https://en.wikipedia.org/wiki/List_of_S%26P_500_companies#S&P_500_component_stocks"

)

df = pd.read_html(link, header=0)[0]

[3]:

df.head()

[3]:

| Symbol | Security | GICS Sector | GICS Sub-Industry | Headquarters Location | Date added | CIK | Founded | |

|---|---|---|---|---|---|---|---|---|

| 0 | MMM | 3M | Industrials | Industrial Conglomerates | Saint Paul, Minnesota | 1957-03-04 | 66740 | 1902 |

| 1 | AOS | A. O. Smith | Industrials | Building Products | Milwaukee, Wisconsin | 2017-07-26 | 91142 | 1916 |

| 2 | ABT | Abbott Laboratories | Health Care | Health Care Equipment | North Chicago, Illinois | 1957-03-04 | 1800 | 1888 |

| 3 | ABBV | AbbVie | Health Care | Biotechnology | North Chicago, Illinois | 2012-12-31 | 1551152 | 2013 (1888) |

| 4 | ACN | Accenture | Information Technology | IT Consulting & Other Services | Dublin, Ireland | 2011-07-06 | 1467373 | 1989 |

[4]:

sym_str = []

for sym in df.Symbol:

# if sym == 'BRK.B': ## some errors with this ticker

# continue

sym_str.append(sym)

[5]:

# np.where(np.array(sym_str) == 'BRK.B')

[6]:

%%time

import yfinance as yf

df = yf.download(sym_str,

start="2000-01-01",

end="2005-11-30")

[*********************100%***********************] 503 of 503 completed

102 Failed downloads:

['OTIS', 'PLTR', 'DAL', 'CZR', 'LULU', 'UBER', 'PODD', 'KVUE', 'NXPI', 'DG', 'MPC', 'MRNA', 'V', 'FTV', 'VICI', 'VLTO', 'NCLH', 'QRVO', 'DELL', 'FTNT', 'CTVA', 'ABNB', 'ENPH', 'SW', 'PAYC', 'LDOS', 'PYPL', 'GEHC', 'FOXA', 'HCA', 'KEYS', 'IR', 'APTV', 'FOX', 'VRSK', 'KHC', 'GEV', 'EPAM', 'CARR', 'CHTR', 'KMI', 'KDP', 'CPAY', 'FANG', 'TEL', 'BX', 'CEG', 'AMCR', 'ABBV', 'CFG', 'LYV', 'VST', 'HLT', 'IQV', 'ZTS', 'MA', 'PSX', 'LW', 'NWSA', 'HPE', 'GNRC', 'PARA', 'TSLA', 'CMG', 'CBOE', 'AMTM', 'DAY', 'PM', 'XYL', 'MSCI', 'AVGO', 'CTLT', 'HWM', 'KKR', 'GM', 'LYB', 'AWK', 'DFS', 'INVH', 'PANW', 'META', 'FSLR', 'CDW', 'DOW', 'BR', 'TRGP', 'SYF', 'CRWD', 'GDDY', 'TDG', 'UAL', 'HII', 'NWS', 'TMUS', 'ALLE', 'SOLV', 'NOW', 'ANET', 'ULTA', 'SMCI']: YFPricesMissingError('$%ticker%: possibly delisted; no price data found (1d 2000-01-01 -> 2005-11-30) (Yahoo error = "Data doesn\'t exist for startDate = 946702800, endDate = 1133326800")')

['BF.B']: YFPricesMissingError('$%ticker%: possibly delisted; no price data found (1d 2000-01-01 -> 2005-11-30)')

['BRK.B']: YFTzMissingError('$%ticker%: possibly delisted; no timezone found')

CPU times: user 10.9 s, sys: 1.43 s, total: 12.3 s

Wall time: 45.3 s

[7]:

df

[7]:

| Price | Adj Close | ... | Volume | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Ticker | A | AAPL | ABBV | ABNB | ABT | ACGL | ACN | ADBE | ADI | ADM | ... | WTW | WY | WYNN | XEL | XOM | XYL | YUM | ZBH | ZBRA | ZTS |

| Date | |||||||||||||||||||||

| 2000-01-03 00:00:00+00:00 | 43.463020 | 0.843077 | NaN | NaN | 8.288178 | 1.215037 | NaN | 16.274673 | 28.214649 | 6.248421 | ... | NaN | 973700 | NaN | 2738600 | 13458200 | NaN | 3033493 | NaN | 1055700 | NaN |

| 2000-01-04 00:00:00+00:00 | 40.142929 | 0.771997 | NaN | NaN | 8.051378 | 1.208433 | NaN | 14.909400 | 26.787292 | 6.183335 | ... | NaN | 1201700 | NaN | 425200 | 14510800 | NaN | 3315031 | NaN | 522450 | NaN |

| 2000-01-05 00:00:00+00:00 | 37.652863 | 0.783293 | NaN | NaN | 8.036577 | 1.320692 | NaN | 15.204174 | 27.178352 | 6.085704 | ... | NaN | 1184600 | NaN | 500200 | 17485000 | NaN | 4642602 | NaN | 612225 | NaN |

| 2000-01-06 00:00:00+00:00 | 36.219181 | 0.715509 | NaN | NaN | 8.317783 | 1.307485 | NaN | 15.328291 | 26.435350 | 6.118246 | ... | NaN | 1307700 | NaN | 344100 | 19461600 | NaN | 3947658 | NaN | 263925 | NaN |

| 2000-01-07 00:00:00+00:00 | 39.237442 | 0.749401 | NaN | NaN | 8.406582 | 1.380124 | NaN | 16.072981 | 27.178352 | 6.215880 | ... | NaN | 1728000 | NaN | 469500 | 16603800 | NaN | 6063647 | NaN | 333900 | NaN |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2005-11-22 00:00:00+00:00 | 21.471949 | 2.004027 | NaN | NaN | 12.146412 | 5.756105 | 19.911514 | 33.459999 | 24.157951 | 15.514473 | ... | 408757.0 | 1194300 | 1844900.0 | 1165200 | 17084900 | NaN | 4531322 | 2415350.0 | 460300 | NaN |

| 2005-11-23 00:00:00+00:00 | 21.520235 | 2.021802 | NaN | NaN | 12.044474 | 5.811047 | 19.681894 | 33.860001 | 23.992666 | 15.584385 | ... | 269573.0 | 583400 | 1241600.0 | 956500 | 12535100 | NaN | 4187466 | 1782003.0 | 346600 | NaN |

| 2005-11-25 00:00:00+00:00 | 21.544378 | 2.088985 | NaN | NaN | 12.041378 | 5.782519 | 20.019140 | 33.910000 | 24.170670 | 15.584385 | ... | 71385.0 | 387000 | 248400.0 | 278900 | 6692600 | NaN | 1553191 | 806284.0 | 78300 | NaN |

| 2005-11-28 00:00:00+00:00 | 21.520235 | 2.098625 | NaN | NaN | 12.032114 | 5.689543 | 19.875635 | 33.209999 | 23.642996 | 15.419132 | ... | 249716.0 | 866800 | 1201400.0 | 961600 | 15008400 | NaN | 3960455 | 2082145.0 | 369200 | NaN |

| 2005-11-29 00:00:00+00:00 | 21.423653 | 2.051627 | NaN | NaN | 11.788074 | 5.592340 | 20.263098 | 32.400002 | 23.687513 | 15.406424 | ... | 484219.0 | 1447800 | 1319400.0 | 1213900 | 18592400 | NaN | 3747632 | 2305346.0 | 375500 | NaN |

1486 rows × 3018 columns

[8]:

df = df.Close

[10]:

df = df.dropna(axis=1)

[11]:

df.describe()

[11]:

| Ticker | A | AAPL | ABT | ACGL | ADBE | ADI | ADM | ADP | ADSK | AEE | ... | WM | WMB | WMT | WRB | WST | WY | XEL | XOM | YUM | ZBRA |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | ... | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 | 1486.000000 |

| mean | 23.861300 | 0.664605 | 20.344236 | 3.293209 | 22.208247 | 44.042129 | 14.695453 | 36.782113 | 14.772824 | 43.275805 | ... | 25.615674 | 16.373156 | 17.748793 | 3.963122 | 8.042779 | 56.940855 | 19.694273 | 43.131734 | 10.797933 | 32.594770 |

| std | 14.722275 | 0.475175 | 2.607677 | 1.213181 | 7.128621 | 15.386976 | 4.234437 | 6.614726 | 11.025208 | 5.389743 | ... | 4.202009 | 10.380676 | 1.424192 | 1.900309 | 2.778387 | 7.526926 | 5.790209 | 7.630408 | 4.161873 | 12.469408 |

| min | 7.761087 | 0.234286 | 13.298689 | 1.270833 | 8.350000 | 18.290001 | 7.916667 | 21.610996 | 4.984375 | 27.812500 | ... | 13.062500 | 0.717376 | 14.163333 | 0.855967 | 4.137500 | 36.687500 | 5.660000 | 30.270000 | 4.268512 | 15.194444 |

| 25% | 15.901288 | 0.340223 | 18.642854 | 1.851111 | 16.902500 | 35.717500 | 12.032500 | 32.202368 | 7.605000 | 40.459844 | ... | 23.812500 | 7.803502 | 16.697500 | 2.473251 | 6.016250 | 50.782499 | 16.497500 | 37.857499 | 7.712527 | 22.313195 |

| 50% | 19.041488 | 0.420268 | 20.186284 | 3.368334 | 20.655001 | 40.254999 | 13.610000 | 35.152567 | 9.265313 | 42.535000 | ... | 26.710000 | 14.498332 | 17.751666 | 3.462058 | 6.803750 | 57.750000 | 18.195001 | 41.258905 | 10.334292 | 27.413333 |

| 75% | 25.041129 | 0.969029 | 22.353882 | 4.308056 | 28.640000 | 47.857500 | 16.665000 | 41.784565 | 18.675000 | 46.054999 | ... | 28.900000 | 26.710028 | 18.686458 | 5.410370 | 9.635625 | 63.500000 | 25.590625 | 45.097499 | 13.588246 | 43.784167 |

| max | 113.733910 | 2.487857 | 25.901581 | 6.255556 | 41.625000 | 101.375000 | 25.320000 | 54.622288 | 47.599998 | 56.290001 | ... | 32.380001 | 36.435467 | 22.833332 | 9.392593 | 14.915000 | 74.125000 | 31.639999 | 64.980003 | 19.166067 | 61.889999 |

8 rows × 352 columns

[101]:

# Compute daily returns

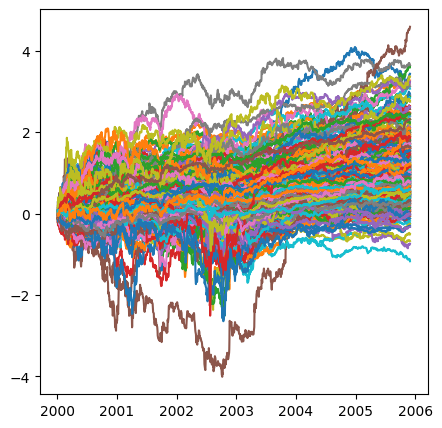

daily_returns = df.pct_change().dropna()

# Compute cumulative returns

cumulative_returns = daily_returns.cumsum()

# Plot cumulative returns

plt.figure(figsize=(5, 5))

plt.plot(cumulative_returns)

plt.show()

[78]:

daily_returns.values[-1].shape

[78]:

(352,)

[84]:

plt.figure(figsize=(5,5))

plt.hist(daily_returns.values[-1],bins=50,density=True,alpha=0.7,color='black');

plt.xlabel("final returns")

[84]:

Text(0.5, 0, 'final returns')

[12]:

from scipy.stats import mode

tickers = sorted(list(set(df.columns.values))) # sorted list of unique tickers

tkrlens = [len(df[tkr][(df.index>df.index[0]) & (df.index<df.index[-1])]) for tkr in tickers] # find lengths of times series for each ticker

tkrmode = mode(tkrlens)[0]

[13]:

# tkrmode,tkrlens

int(tkrmode)

[13]:

1484

[14]:

# idenfity tickers whose lenghts equal the mode and call these good tickers

good_tickers = [tickers[i] for i,tkr in enumerate(tkrlens) if tkrlens[i]==int(tkrmode)]

[15]:

len(good_tickers)

[15]:

352

[34]:

import numpy as np

import pandas as pd

rtndf = pd.DataFrame() # initialize a return dataframe

std_lst = [] # list of standard deviations of return time series

# Initialize containers for results

std_lst = []

normalized_returns = []

# Loop through tickers

for tkr in good_tickers:

# Select relevant data for the current ticker

tmpdf = df[tkr][(df.index > df.index[0]) & (df.index < df.index[-1])]

# Compute returns

tmprtndf = ((tmpdf - tmpdf.shift(1)) / tmpdf).dropna()

# Compute and store standard deviation of returns

std_lst.append(np.std(tmprtndf))

# Normalize returns to have mean 0 and std 1

rsdf = (tmprtndf - tmprtndf.mean()) / tmprtndf.std()

# Collect normalized returns

normalized_returns.append(rsdf)

# Combine all normalized returns into a single DataFrame

rtndf = pd.concat(normalized_returns, axis=1)

# Assign column names for clarity

rtndf.columns = good_tickers

[35]:

rtndf = rtndf.dropna(axis=1)

[36]:

rtndf

[36]:

| A | AAPL | ABT | ACGL | ADBE | ADI | ADM | ADP | ADSK | AEE | ... | WM | WMB | WMT | WRB | WST | WY | XEL | XOM | YUM | ZBRA | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2000-01-05 00:00:00+00:00 | -1.652114 | 0.339111 | -0.094890 | 4.533024 | 0.494402 | 0.391044 | -0.863298 | -0.469242 | -2.154160 | 2.964119 | ... | 0.171534 | 0.939150 | -1.043349 | -0.959997 | -0.222766 | 2.522511 | 1.329485 | 3.275063 | 0.217536 | 0.656975 |

| 2000-01-06 00:00:00+00:00 | -0.976707 | -2.213384 | 1.784607 | -0.590885 | 0.209925 | -0.698878 | 0.260417 | 0.668884 | -2.079548 | -0.320116 | ... | -0.371835 | 0.354974 | 0.568648 | 2.964085 | -0.550886 | 2.241927 | -0.318732 | 3.113565 | -0.420512 | -2.002760 |

| 2000-01-07 00:00:00+00:00 | 1.987224 | 1.059422 | 0.559123 | 2.789052 | 1.173289 | 0.723180 | 0.806858 | 1.120238 | 3.345925 | 1.160135 | ... | -2.088760 | 0.433407 | 3.599164 | -0.924117 | 0.529835 | -1.686104 | 0.013379 | -0.197399 | -1.084342 | -0.392793 |

| 2000-01-10 00:00:00+00:00 | 1.483355 | -0.416753 | -0.371708 | 1.699401 | 0.942561 | 2.075901 | -0.019386 | 1.207366 | -0.405292 | -0.615250 | ... | 0.179665 | -0.267385 | -0.928873 | -0.586748 | 1.045775 | -0.207362 | 0.013379 | -0.911440 | 1.788797 | 1.139295 |

| 2000-01-11 00:00:00+00:00 | -0.320440 | -1.258685 | -0.756382 | 0.447644 | -1.854867 | -1.075436 | -0.858814 | -0.971833 | -0.877784 | -0.169490 | ... | -0.580316 | -0.151340 | -0.750856 | -0.945843 | -1.525405 | -0.518909 | 0.013379 | 0.178791 | -0.337250 | 0.238076 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2005-11-21 00:00:00+00:00 | 0.081205 | 0.145864 | -0.689956 | 0.268425 | -0.122601 | 0.307816 | -0.105377 | -0.269489 | 1.524217 | 0.196095 | ... | 0.317202 | 0.226646 | 0.141722 | -0.009257 | -0.231146 | 0.531092 | -0.314097 | 1.188517 | 0.274958 | 0.759514 |

| 2005-11-22 00:00:00+00:00 | 0.452270 | 0.550249 | -1.405676 | -0.284010 | 0.103800 | 0.231241 | -0.148685 | -0.494847 | 0.940656 | 0.318441 | ... | -0.419457 | 0.374999 | 0.607321 | 0.819670 | -1.212837 | 0.224354 | 0.224016 | 0.298565 | 0.197704 | 0.075627 |

| 2005-11-23 00:00:00+00:00 | 0.087384 | 0.207454 | -0.444021 | 0.462745 | 0.303559 | -0.154691 | 0.216604 | -0.199132 | -0.604925 | 0.606260 | ... | -0.173555 | -0.370975 | 0.391365 | 0.245149 | -0.258263 | -0.488602 | 0.560124 | 0.212561 | 0.374536 | 0.067912 |

| 2005-11-25 00:00:00+00:00 | 0.058808 | 0.753891 | -0.011320 | -0.312457 | 0.043060 | 0.210892 | -0.019386 | 0.309780 | -0.315012 | 0.736627 | ... | -0.008719 | 0.293798 | -0.062294 | -0.173453 | 0.406501 | -0.058102 | 0.200910 | 0.243391 | -0.543512 | 0.007384 |

| 2005-11-28 00:00:00+00:00 | 0.001752 | 0.109287 | -0.038407 | -0.927121 | -0.525170 | -0.550410 | -0.583155 | -0.748739 | 0.196496 | 0.145696 | ... | -0.340571 | -0.552984 | -0.481010 | -0.526534 | -0.806800 | 0.080393 | 0.050847 | -1.492546 | 0.027047 | -0.592475 |

1483 rows × 352 columns

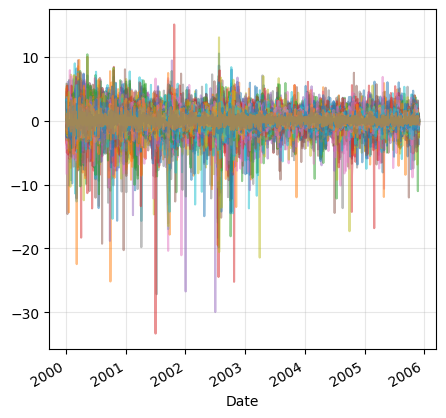

[102]:

rtndf.plot(figsize=(5,5),alpha=0.5,legend=False);

plt.grid(alpha=0.3);

plt.show();

[20]:

rtndf.columns = good_tickers

cmat = rtndf.corr() # compute correlation matrix

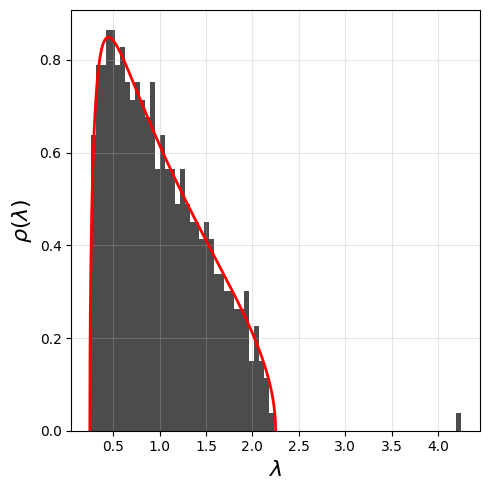

evls, evcs = np.linalg.eig(cmat) # compute eigenvalue/vector decomposition of matrix

[21]:

N = len(evls)

T = len(rtndf)

q = N/T

Q = 1/q

print(N,T,q,Q)

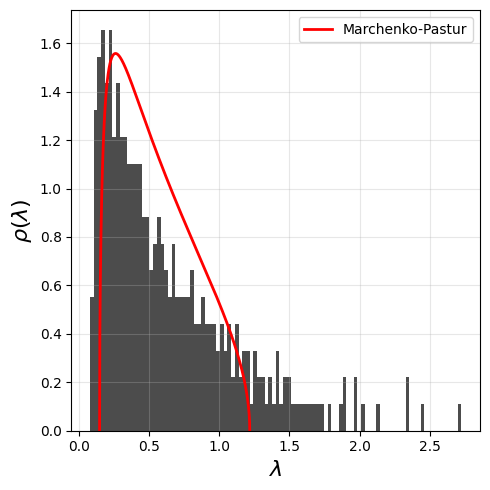

352 1483 0.23735670937289277 4.213068181818182

[33]:

import matplotlib.pyplot as plt

# plt.hist([val for val in evls if val < 1.5],bins=50,density=True);

# Plot Marchenko-Pastur distribution

sig2 = 0.55

lambda_plus = (1 + np.sqrt(q))**2*sig2

lambda_minus = (1 - np.sqrt(q))**2*sig2

x = np.linspace(lambda_minus, lambda_plus, 1000)

mp_density = (1 / (2 * np.pi * q * x * sig2)) * np.sqrt((lambda_plus - x) * (x - lambda_minus))

plt.figure(figsize=(5,5))

plt.plot(x, mp_density, 'r-', lw=2, label='Marchenko-Pastur')

plt.legend()

_ = plt.hist( evls[evls<3] ,bins=100,density=True,color='black',alpha=0.7)

# plt.yscale('log')

plt.xlabel(r"$\lambda$",fontsize=16)

plt.ylabel(r"$\rho(\lambda)$",fontsize=16)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

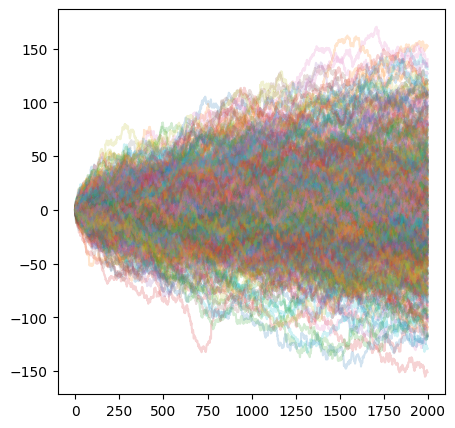

16.4.2. Market simulation¶

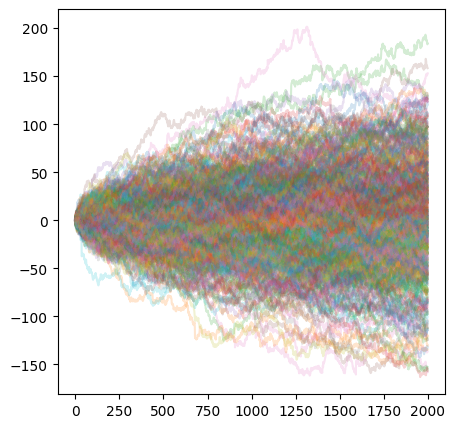

Simulate daily return time series drawn from a heavy tailed distribution. We chose the Student’s t distribution with degree of freedom parameter 5.

Let us simulate \(N=500\) stocks over \(T=2000\) trading days.

[100]:

import matplotlib.pyplot as plt

import numpy as np

deg_freedom = 5 # Student's t distribution degree of freedom parameter

num_srs = 500 # number of time series to generate

num_pts = 2000 # number of points per time series

rpaths = np.random.standard_t(deg_freedom,size=(num_pts,num_srs)) # generate paths

evalplot = np.linalg.eig(pd.DataFrame(rpaths).corr())[0] # compute eigenvalues

plt.figure(figsize=(5,5))

_ = plt.plot(rpaths.cumsum(axis=0),alpha=0.2)

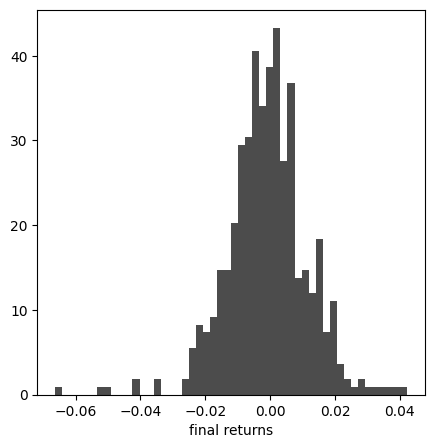

[75]:

rpaths[-1].shape

[75]:

(500,)

[80]:

plt.figure(figsize=(5,5))

plt.hist(rpaths[-1]/100,bins=50,density=True,alpha=0.7,color='black');

plt.xlabel("final returns")

[80]:

Text(0.5, 0, 'final returns')

[90]:

plt.figure(figsize=(5,5))

plt.hist(evalplot,bins=75,density=True,color='black',alpha=0.7);

# Marchenko-Pastur parameters

Q = num_pts / num_srs # Aspect ratio

print(Q)

lambda_plus = (1 + np.sqrt(1 / Q))**2

lambda_minus = (1 - np.sqrt(1 / Q))**2

x = np.linspace(lambda_minus, lambda_plus, 1000)

def marchenko_pastur_pdf(x, q):

"""Marchenko-Pastur probability density function."""

return (Q / (2 * np.pi)) * np.sqrt((lambda_plus - x) * (x - lambda_minus)) / x

# Compute Marchenko-Pastur density

mp_pdf = marchenko_pastur_pdf(x, q)

plt.plot(x, mp_pdf, color='red', lw=2, label='Marchenko-Pastur')

plt.xlabel(r"$\lambda$",fontsize=16)

plt.ylabel(r"$\rho(\lambda)$",fontsize=16)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

4.0

Simulation with market mode

[93]:

import matplotlib.pyplot as plt

import numpy as np

deg_freedom = 5 # Student's t distribution degree of freedom parameter

num_srs = 500 # number of time series to generate

num_pts = 2000 # number of points per time series

# Generate random paths

rpaths = np.random.standard_t(deg_freedom, size=(num_pts, num_srs))

market_influence = 0.1 # Strength of the market influence

# Generate a market factor (common mode)

market_factor = np.random.normal(0, 1, size=(num_pts, 1))

# Add market influence to each path

rpaths_with_market = rpaths + market_influence * market_factor

# Compute the correlation matrix and its eigenvalues

correlation_matrix = pd.DataFrame(rpaths_with_market).corr()

evalplot = np.linalg.eig(correlation_matrix)[0] # Eigenvalues

[98]:

plt.figure(figsize=(5,5))

_ =plt.plot(rpaths_with_market.cumsum(axis=0),alpha=0.2)

[95]:

plt.figure(figsize=(5,5))

plt.hist(evalplot,bins=75,density=True,color='black',alpha=0.7);

# Marchenko-Pastur parameters

Q = num_pts / num_srs # Aspect ratio

print(Q)

lambda_plus = (1 + np.sqrt(1 / Q))**2

lambda_minus = (1 - np.sqrt(1 / Q))**2

x = np.linspace(lambda_minus, lambda_plus, 1000)

def marchenko_pastur_pdf(x, q):

"""Marchenko-Pastur probability density function."""

return (Q / (2 * np.pi)) * np.sqrt((lambda_plus - x) * (x - lambda_minus)) / x

# Compute Marchenko-Pastur density

mp_pdf = marchenko_pastur_pdf(x, q)

plt.plot(x, mp_pdf, color='red', lw=2, label='Marchenko-Pastur')

plt.xlabel(r"$\lambda$",fontsize=16)

plt.ylabel(r"$\rho(\lambda)$",fontsize=16)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

4.0

The SP500 correlation looks very much like a Marchenko Pastur distribution, plus some information (or signal). To extract the non-noisy part of the stock correlation, we could fit the Marchenko Pastur distribution to the empirical eigenvalues and remove the eigenvalues that are compatible with the Marchenko Pastur distribution.

With this idea, we can denoise the correlation matrix, and hope to build robust portfolios. To learn more about this you can read A First Course in Random Matrix Theory, Potters & Bouchaud (2020).

16.5. Application to Medical Imaging¶

In vivo imaging of the brain tissue has been revolutionized by the development of diffusion Magnetic Resonance Imaging (dMRI) and tractography. Thermal noise corrupts dMRI measurements and propagates to the quality of the reconstructed images, hampering it.

In 2016, Veraart et al. proposed a denoising method based on the Marchenko Pastur distribution, which fast and optimal in the sense that it provides an optimal compromise between noise suppression and loss of anatomical information.

The method is called the Marchenko Pastur Principal Component Analysis denoising algorithm and is implemented in the DIPY package. See here.

The idea is to construct a data matrix \(\tilde{\mathbf{H}}\) based on the original matrix after nullifying all eigenvalues that are smaller than the \(\lambda_+\) predicted by the Marchenko Pastur distribution (i.e., the pure-noise eigenvalues). This is a prametric denoising method, where both the noise level \(\sigma^2\) and the number of principal components \(P\) are estimated from the data.

The reduction in noise is given by

where \(P\) is the number of principal components that are retained and \(N\) the dimension of the data vector. (The number eigenvalues described by the Marchenko Pastur distribution is \(N-P\), they correspond to those that are nulled.)

See Denoising of diffusion MRI using random matrix theory, Veraart et al. (2016) for details.

16.6. Application to Learning Algorithms¶

Refer to Random Matrix Methods for Machine Learning, Couillet & Liao (2023) and the online ICML tutorial: Random Matrix Theory and Machine Learning.